Posted on October 28, 2020 by IAC Desk in Metals

China’s imports of steel semis over January-August skyrocketed ten folds on year to a total of 11.4 million tonnes, according to data from China’s General Administration of Customs (GACC), and the surge contributed greatly to China’s re-emergence as a net steel importer during June-August for the first time in over a decade.

For this year, the rather “abnormal phenomenon” has had to do with the chaos created by the COVID-19, as the pandemic has thrown many economies into the dark hole while China, being the first to have experienced the blow, has been the only one that have seemingly climbed out and returned to the normal track since March, being the only buyer of excess steel from the other countries for a while.

The question, thus, wanders in the air that whether this will be a one-off phenomenon or a new occurrence that will emerge in the Chinese steel market whenever it is profitable to do so for both the traders and the steel producers.

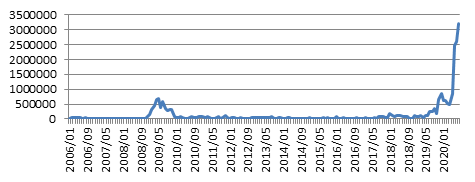

China’s steel semis imports hit a record high

Since July, the volume of semi-finished steel items such as slabs and billets being imported into China has been breaking existing records. By August, the monthly import volume had hit 3.2 million tonnes, up 23.4% on month or by a huge 1,131% on year, with billets taking about half.

The August result was in stark contrast to China’s average monthly import volume of semis during 2013-2019 of less than 300,000 tonnes, and even during this year’s January-May period, when COVID was ravaging the Chinese economy, and the average volume was slightly above 500,000 tonnes/month, according to the GACC data.

China’s Steel Semis Imports Over 2006-2020 (unit: t)

Within the 11.4 million tonnes of semis that arrived in China over January-August, common-grade carbon steel billets reached 6.1 million tonnes, or 54% of the total, which was up 301% from the whole 2019, slabs accounted for around 37% of the total at 4.2 million tonnes, which was also nearly four times of the last year’s total imports of slabs, and the remainders were high-carbon semis, stainless steel semis, and other alloy semis, Mysteel Global understands.

Broadening price gap opens import window amid COVID-19

The broadening price gap of the steel semis between China and its foreign peers with China’s earlier recovery from COVID-19 is understood as the key factor for the soaring steel imports, Mysteel Global understands from industry sources.

“Thanks to the effective measures, the pandemic has been successfully contained in China, enabling the economy and steel consumption to steadily revive, whereas the countries such as India are still battling hard against the virus, and their steel mills have had to lower steel prices to fight for the Chinese market so as to ease the supply pressure domestically,” said a Shanghai-based senior analyst.

“Over April-May, overseas semis offering prices in FOB were about Yuan 500-800/tonne ($74.6-119.4/t) lower than China’s domestic supplies, and the difference, even taken into account of import tariffs and logistics costs, were still quite competitive, and many Chinese steel re-rollers and traders had booked actively as a result,” she added.

Billet offers from CIS countries over April-May averaged $345.3/tonne FOB via the Black Sea, or equivalent to around Yuan 2,889/t including 13% VAT, a 2% tariff and a $30/t freight, while the Tangshan billet price in North China was at Yuan 3,126.8/t EXW and including the 13% VAT back then, according to Mysteel’s data.

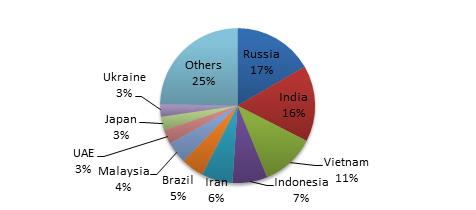

China charges no duties on steel semis imported from the ASEAN countries but will collect a 2% tariff from the semis imported elsewhere, Mysteel Global understands, but even so, Russia and India still scored the top two steel semis suppliers to China with the volumes at 2.27 million tonnes and 2.16 million tonnes respectively, according to the GACC data.

China’s Jan-Aug Carbon Steel Semis Imports by Country

China’s steel imports show signs of a trend in forming

Even without the COVID-19, China’s steel semis would still have been on the rise this year though at a much milder rate, as China’s overseas steel investments have been on the surge especially in the ASEAN region and when commissioned, the products, other than fulfilling the domestic needs, may flow back to China, the world’s top steelmaking and steel consuming country, the analyst noted, and in reality, ASEAN region has seen its steel exports to China grow since 2017.

Internally, China’s steel producers have reduced their semis supply to the market, and in the first quarter, for example, China’s domestic semis supply declined 2.1 million tonnes on year due to COVID-19, according to Mysteel’s tracking.

The supply recovered moderately over April-June with resumption of normal economic orders and nationwide transportation, but the permanent exit of 15 steel producers of the total 18 mills in Xuzhou of East China’s Jiangsu province as part of the industrial integration led to the supply gap in the region, as Mysteel Global reported.

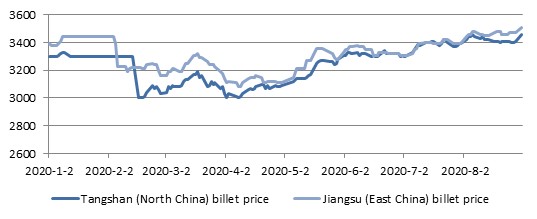

Robust demand from the re-rollers across China and the only Yuan 100-150/t price difference of the Q235 150mm square billet in Tangshan, North China’s Hebei against that in Jiangsu, making it no longer “attractive” for users in East and South China to ship from North China at a transportation cost of Yuan 200/t, and the local re-rollers would rather seek lower-priced imported semis.

Billet Prices in Tangshan and Jiangsu (unit: Yuan/t)

Most semis imported to East China, mainly for longs rolling

Hence, it was no surprise that Zhejiang, Jiangsu, and Shanghai in East China, together with Fujian in Southeast China, received around 90% of China’s imported semis over January-August, especially as most of them are along the country’s coastal lines, making it convenient to receive long-haul vessels, and many large-sized steel trading houses in China such as Hangzhou CIEC International Co and Zheshang Development Group Co. had been rather active parties in the steel trade.

Arrivals of Semis Imports over Jan-Aug by region

| Province/Municipality | Region | Jan-Aug semis arrivals (‘000 t) | Proportion |

| Zhejiang | East China | 5,784 | 50.9% |

| Jiangsu | 2,546 | 22.4% | |

| Fujian (Southeast China) | 1,438 | 12.6% | |

| Shanghai | 458 | 4% | |

| Beijing | North China | 223 | 2% |

| Tianjin | 221 | 2% | |

| Hebei | 189 | 1.7% | |

| Xinjiang | Northwest China | 156 | 1.4% |

| Liaoning | Northeast China | 90 | 0.8% |

| Hunan | Central China | 76 | 0.7% |

Mysteel’s survey showed that the imported billets over January-August had been rolled into rebar, wire rod and section, with rebar consuming around 80% and wire rod 10%, and 85% of the imported slabs were for medium plate production, and all the imported semis, thus, contributed to a majority of the added output for such finished steel products.

Over April-September, China’s rebar output increased 8.6 million tonnes on year, among which, the domestic integrated mills contributed to 4.2 million tonnes, while re-rolling with the imported semis took care of 4.25 million tonnes or 49.4% of the total, according to Mysteel’s survey when China’s steel market had been back to the normal track.

Over the same period, China’s medium plate output grew 3.45 million tonnes on year, among which around 2.9 million tonnes or 84.2% was rolled by the imported slabs, Mysteel noted.

2020 may be a “unique” year in many aspects, but China’s high steel imports especially when the steel production costs have been running high, indeed, may have triggered the market participants’ change of perspective when viewing the world’s largest steel base.

For this year, the complaints on China’s too high steel exports have been fading away, while more overseas steel traders and steel mills have been reassessing the market and trying to build up their steel exports channels to China, Mysteel Global noted.

Post time: Oct-30-2020